Data Science and Machine Learning

Buy2Sell, converting collectors to sellers in an online marketplace

a project completed during my

Insight Data Science fellowship

Covetly suffers from the high variance of inventory levels across categories. To add inventory for categories in shortage, the client expects this project to suggest a list of collectors who can be prompted to sell. This project:

- Consolidated 7 Million user behavior records from client’s MongoDB and MSSQL databases

- Used supervised learning classification to recommend potential sellers with 80% confidence level

- Built a dashboard with real-time updates with Dash and Flask deployed on AWS EC2 and cache data stored on AWS RDS

Metal/nonmetal Classification and Bandgap Prediction

a research project completed during my Ph.D. in Materials Science at the

University of Delaware

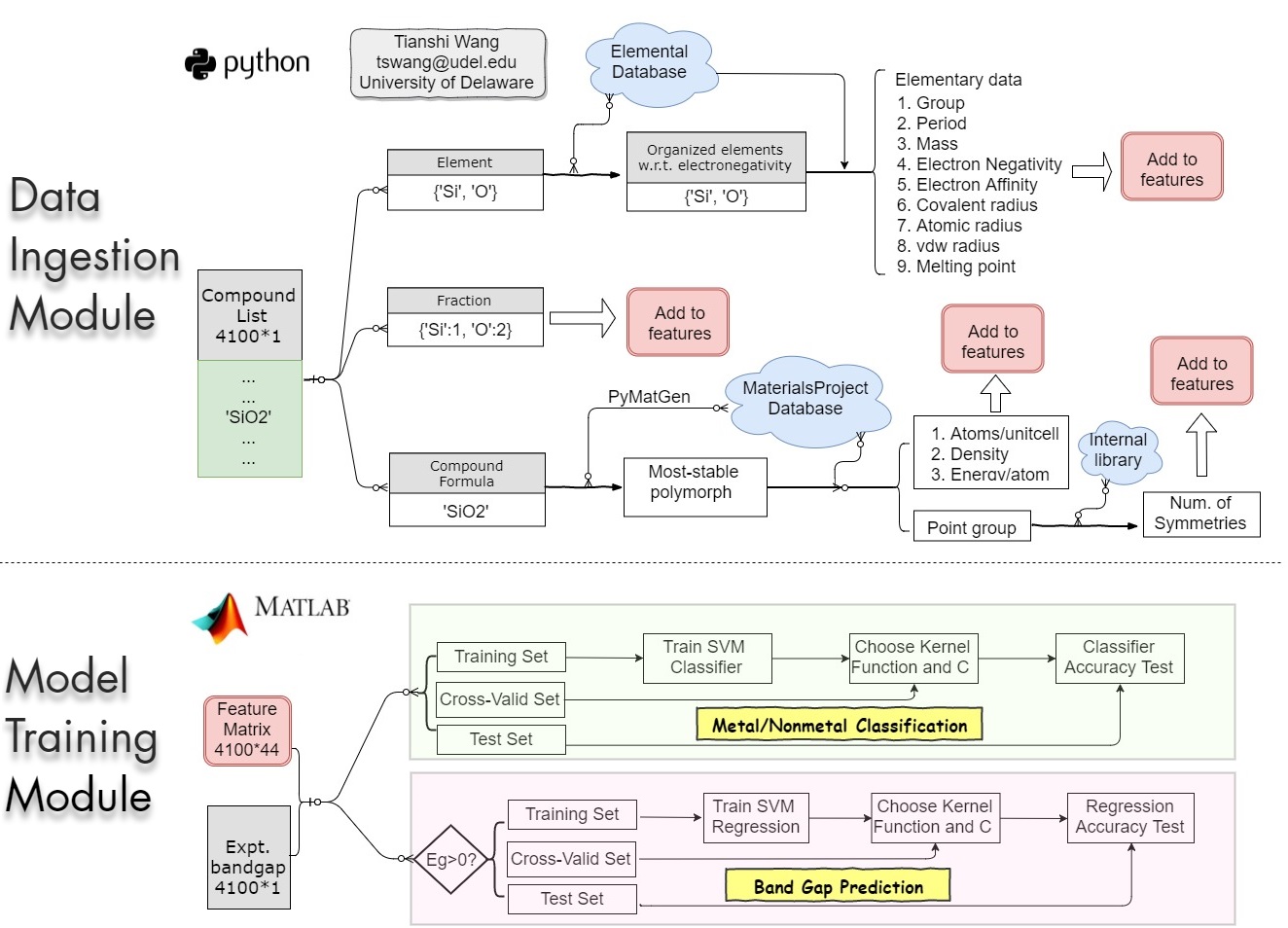

The workflow below shows how the code works for classifying metal/nonmetal and predicting band gaps.

The data ingestion module collects 44 features for each of the ~4100 materials from databases such as

MaterialsProject . Then, the collected data is used to train support vector machine (SVM) classifier and

SVM regression. Finally, we test the models on test set. The result shows the trained model can separate

metal/nonmetal with an accuracy of ~90% and the bandgap prediction accuracy (RMSE = 0.7 eV) outperforms

DFT-LDA calculations.

Workflow of the developed code for metal/nonmetal classification and bandgap projection

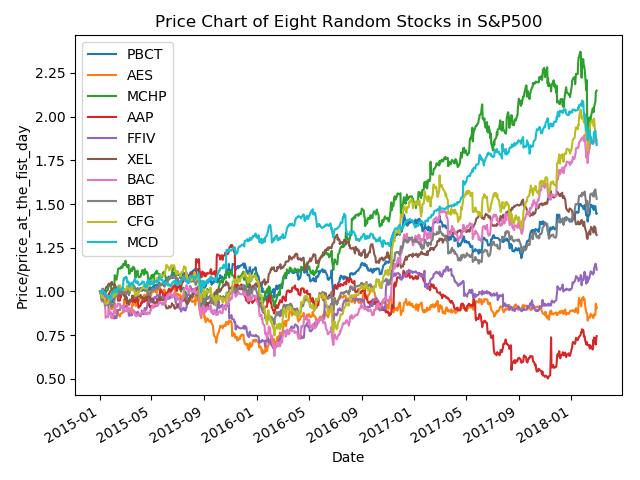

Stock Clustering and Selection from S&P500

This algorithm assumes stocks which performed similarly in the past will likely continue doing so in the near future. Therefore, it is regarded as a buy single if a stock performed worse than others in a cluster. S&P500 stocks are clustered by their daily performance from 201401 to 201801 using KMeans method. Based on their performance during 201802-201805, ~40 underperformed (to-buy) and outperformed (to-sell) stocks are selected. The selected to-buy stocks return 2.2% in 201806 (or 26% annually) compared to 0.5% for market and -0.6% for to-sell stocks.

Diagram of stock-selection procedure using this algorithm

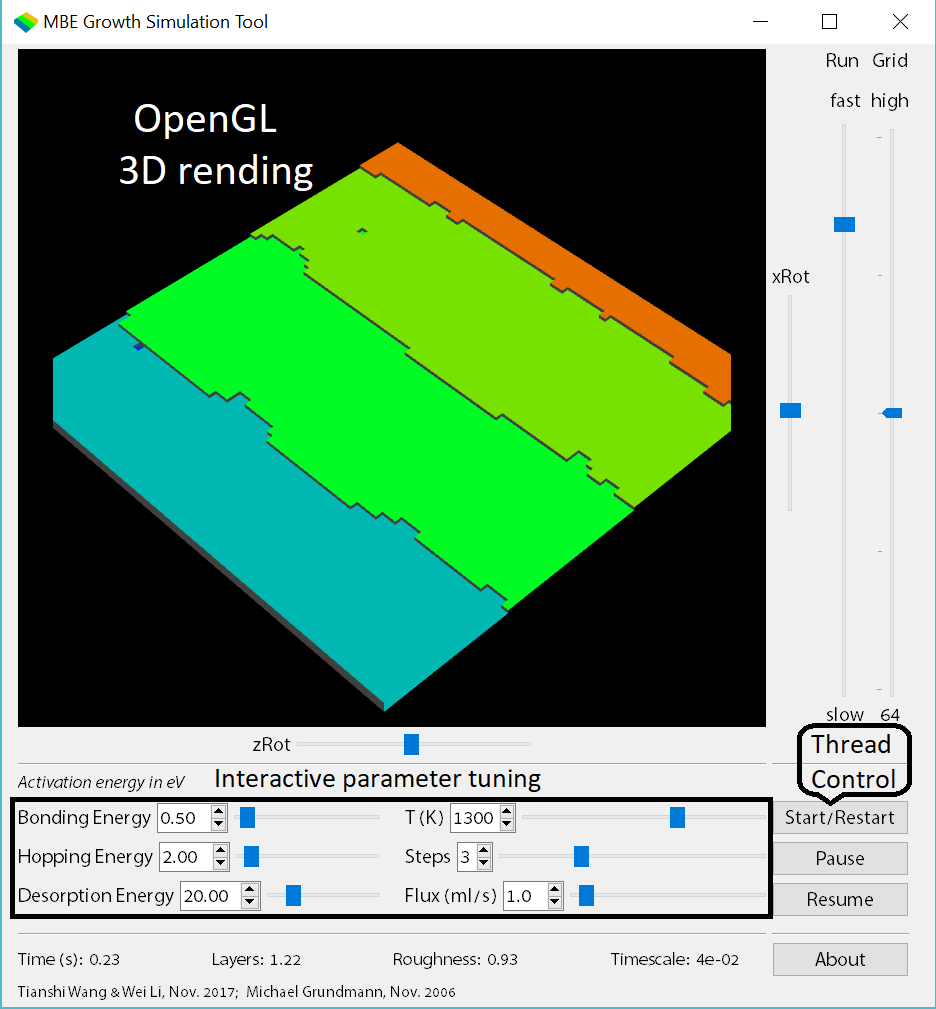

Software Development

Code development to solve real-world problems is important for me. In addition, I have gained experiences of large-scale scientific computing using clusters e.g. SDSC Comet and UTexas Stampede. In the below example, I demonstrate a code which I and Wei Li developed for simulation of epitaxial growth process in molecular beam epitaxy (MBE). Using this code, you can observe different growth morphologies: statistically roughing, step-flow, and islanding by tuning the input parameters. The code was first written in Python and Cython by us based on the KMCInterative code. However, to increase running speed, we finally wrote it in C++ using QT and OpenGL libraries.